Barcelona Dreaming…. the Bull Market in Credit Rolls On

March 31, 2026

(©)

Scroll Down

Neu Capital recently attended the annual Global ABS Conference in Barcelona (along with 5000 other attendees).

The list of attendees included investors (banks, credit funds asset managers), originators, and service providers.

The overwhelming theme this year was the volume of money looking to be deployed.

This was driven by various factors:

- Last year’s concerns about poor credit performance due to the impact of higher rates (from Central Bank tightening) have been proven incorrect, primarily due to sound economic performance across all major geographies and relatively low unemployment.

- The higher base rates have lifted the absolute returns available for real money investors, noting these returns look like longer run equity returns.

- Institutional and HNW investors continue to increase their allocation to the credit sector, across both private and public deals.

- The growing global balance of superannuation funds in accumulation phase underpins the volume of money to be deployed.

Other key themes or areas of debate/discussion:

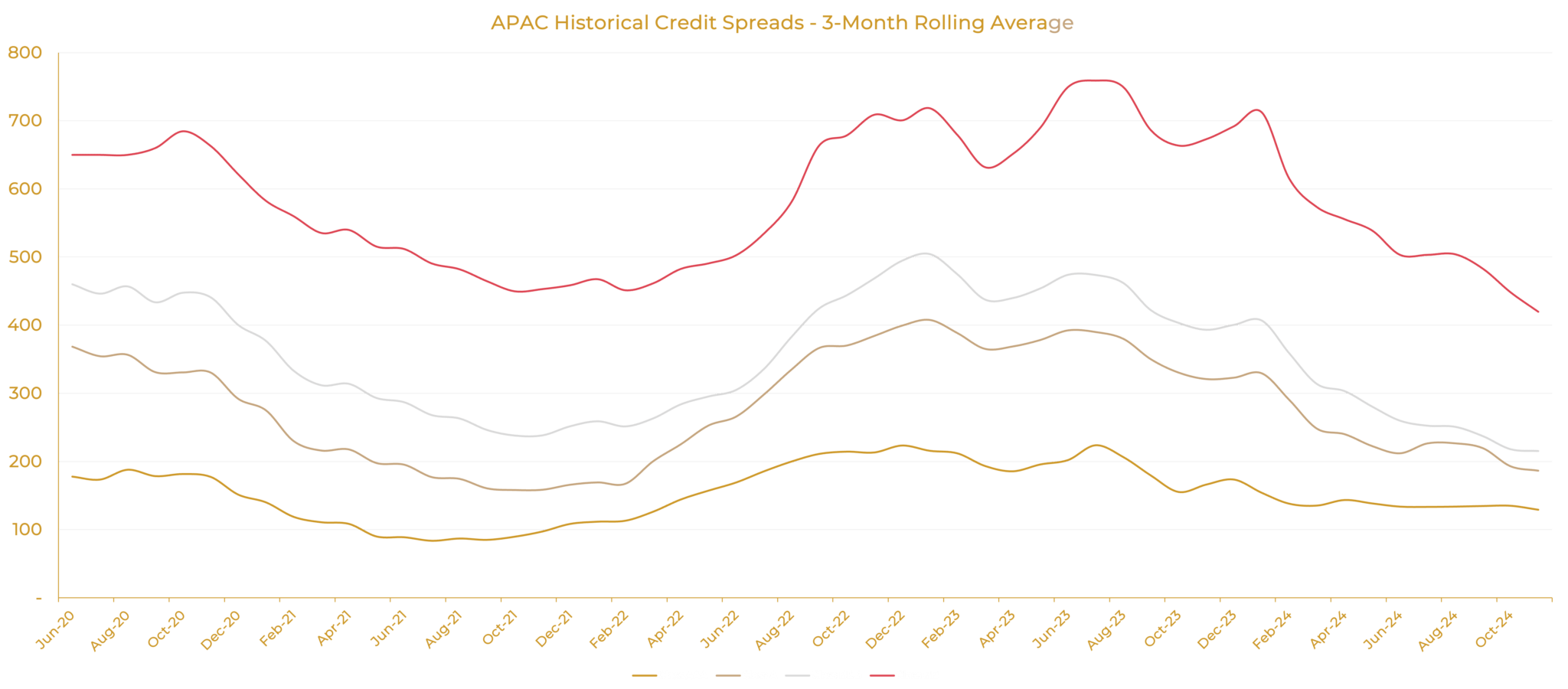

- The volume of money coming into the sector has seen credit spreads rally (contract) at all parts of the curve. There was much discussion about how far margins have rallied and whether there is more room for compression over the remainder of 2024.

- Demand for non-investment grade debt. This debt has rallied significantly, despite the headwinds which are appearing in some economies as the impact of higher base rates (and lending rates) bites consumers and businesses. This is partly driven by credit funds with hurdle returns who are being forced down the credit ladder to meet these hurdles.

- Volume of issuance. Global markets are on track to meet record issuance levels, as both banks and non-banks continue to use securitisation and CLO structures to fund their loans. The generally accepted position was second half issuance would not slow as lenders sort to bring forward their public issuance to optimise the current spread environment, and the demand for debt would support the issuance without materially impacting margins.

- Banks are not reducing their “minimum cheque size”, thereby potentially lengthening the timeframe at which non-banks can achieve bank funding. Whilst we have seen this theme in Australia with NAB/Westpac less aggressive on funding non-banks, this theme appears consistent in Europe.

For any further insights on the Conference, please reach out to John Powell or Ed Jones.

So what’s in store for 2025?

Will the record inflows into credit, both directly and via CIO allocations, continue?Will credit spreads continue to rally?

What will a change in the US Presidency bring (that hasn’t already been priced in)?Can the consumer and SMEs keep hanging tough?

Will the lift in bank and fund manager share prices in 2024 spill over into non-bank lender valuations, or will their share prices remain subdued?

Will we see a major market wobble, and if we do, what will be the catalyst and where will the casualties occur?

We have some views on all of these so please reach out if you’d like to discuss our thoughts on why the rally in credit spreads probably has further to run.

Related Articles

(#)

.png)